From debt stressed to financially free in less than 60 months*

Debt Counselling & Debt Review South Africa

With Debt Counselling you will get financial freedom and stop creditor harassment today. Our highly rated and experienced team will reduce your monthly debt payments into one affordable instalment.

Why Choose Us

Any company can say that they are the best, but we believe that our clients are the ones who should make that decision. For a clear picture of our service and results, listen to the Debt Review with Dummies episode where one of our previous clients shares his experiences.

Listen Here

We are at the top of our industry for these compelling reasons:

Nadia de Weerdt, our Head Counsellor, expertly leads DCASA’s Western Cape branch, ensuring leadership you can trust. We are fully NCR registered and our performance speaks for itself:

We’ve been a top-ten nominee for three years running, and in 2024, we proudly ranked in the Top Five debt counselling companies in South Africa in our tier.

Finally, our consistently strong Hellopeter reviews speak to the high quality of service our clients receive.

Join the SDC family and get the best service in the industry, guaranteed.

National Debt Counsellors

We serve clients across South Africa and bring almost 14 years of financial industry experience.

Skilled and Experienced

Our counsellors are accredited and seasoned. That keeps your debt restructuring on track.

Simple Application

Our assessment and application processes are quick and easy. You will be protected within a few hours.

Here When You Need Us

We’re not open 24/7, but we do have a dedicated WhatsApp line for urgent issues, should the need arise.

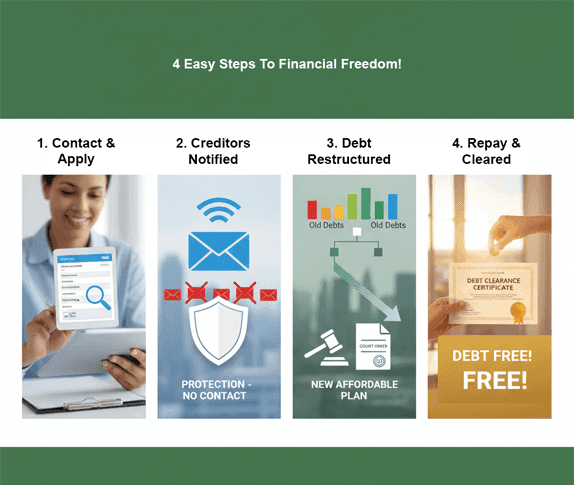

The Debt Review Process in 4 Steps

Apply with a registered Debt Counsellor

- Contact a registered Debt Counsellor.

- Complete Form 16 so they can assess your income, expenses, and debts.

Creditors are notified

- Within 5 business days, the counsellor alerts all creditors and the credit bureaus.

- For 60 business days, creditors may not contact you or start legal action.

Restructure your debt

- The counsellor reviews your budget and negotiates one affordable repayment plan.

- The plan goes to the Magistrate’s Court. Once it becomes a Court Order, it binds you and your creditors.

Repay and get cleared

- Pay one monthly amount to a Payment Distribution Agency (PDA). The PDA pays your creditors under the Court Order.

- After all listed debts are settled, you get a Clearance Certificate. Credit bureaus update your record, and you are debt-free.

Benefits of debt Counselling

Stop legal action and repossession

After you apply and a court order is granted; creditors must stop legal steps. During the initial review, before any action starts, they must also hold off. No new judgments, garnishee orders, or repossessions of your home or car. The National Credit Act gives you this legal protection.

End creditor harassment

Your registered debt counsellor (DC) becomes the point of contact. Creditors must speak to the DC, not you. The calls and emails stop, so you can focus on recovery.

Reduced monthly payments

Your DC negotiates lower instalments you can afford. The plan covers rent, food, transport, and other basics first. You get fast relief.

Lower interest rates

The counsellor proposes reduced rates, especially on unsecured credit like cards and personal loans. You pay less over time and finish sooner if you increase your instalments.

One payment each month

You pay one amount to a Payment Distribution Agency. The PDA pays all listed creditors. Your budget gets simpler, and admin drops.

Clear plan to become debt-free

Debt review follows the National Credit Act. You get a realistic budget and a repayment plan with a clear timeline.

Clearance certificate

When listed short-term debts are settled, or long-term debts like a home loan are up to date, your counsellor issues a clearance certificate. Credit bureaus remove the debt review flag, and you can rebuild your credit record.

Meet Our Head Debt Counsellor

As the Western Cape NEC member for the Debt Counsellors Association, Nadia is very well known in the industry. She has always been drawn to helping people.

She co-owns the SDC Group of which she became Financial Director in 2013 and learned debt review in a hands-on way. She completed the debt counselling course in November 2018.

Nadia blends law, psychology, technology, and mathematics. Debt review is a natural fit and drives her client advocacy. At SDC, she does more than resolve debt. She works to earn consumer trust and teach every client their rights. The firm backs this with a clear, no nonsense promise to protect those rights in every case she oversees.

Your Top 7 Debt Review Questions Answered

It’s normal to feel stressed when facing debt. That’s why we’ve answered the most frequently asked questions about debt review to give you complete confidence. If you need immediate, personalized answers, don’t hesitate, click the link to start your free debt assessment.

What debts can be included in debt review

Most credit agreements under the National Credit Act can be included. This covers:

- Credit cards, store cards, and overdrafts

- Personal loans, payday loans, and microloans

- Vehicle finance

- Home loans

Items usually not included:

- SARS tax debt, traffic fines, and maintenance

- Municipal rates and utilities

- Student debt like NSFAS

- Debts where legal action started before you applied

Will I lose my car or home under debt review

No, the process is designed to protect your assets. You keep them if you pay the restructured amount on time and keep required insurance. You can still lose them if:

- Legal action on that account started before you entered debt review

- You miss payments under the court order

- You choose to sell to settle unaffordable debt

What is debt counselling

Debt counselling is a legal process in South Africa under the National Credit Act. A registered debt counsellor reviews your credit, creates an affordable repayment plan, and applies to court or the consumer tribunal to make that plan an order. While under the plan, credit providers must work with the new terms and you stop taking on new credit.

What is debt review

Debt review is the process you enter after applying for debt counselling. Your accounts are restructured into one monthly payment, interest and fees are reduced where agreed, and creditors listed in the plan cannot take legal action on those debts while you pay as ordered. You finish debt review when you receive your clearance certificate.

How long does debt review last

Debt review usually lasts between 36 to 60 months. It can be shorter if you settle faster, or longer if your budget needs more time. You exit when the debt counsellor issues a clearance certificate after all listed short-term debts are settled, and your home loan is up to date if it was included.

What is a debt counsellor

A debt counsellor is a person registered with the National Credit Regulator. They assess if you are over-indebted, negotiate lower instalments and interest where possible, and prepare the court or tribunal application. They also work with a Payment Distribution Agency to pay your creditors each month.

How much does debt review cost

The National Credit Regulator sets fee guidelines for debt counsellors. Current fees are:

Application and administration: R350 + VAT

Restructure fee: equal to your first month’s instalment, capped at R8,000 + VAT

R9,000 + VAT cap for joint applications married in community of property

Monthly Aftercare Fee: 5% of your instalment, capped at R450 + VAT

These fees are included in your plan and deducted from your monthly payment.

There is a separate legal fee paid to the attorneys who obtain the court order that protects you during debt review. Your debt counsellor will confirm this amount in your application.

Check our latest Articles

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Arcu, porttitor nisi faucibus lorem urna. Condimentum risus non magna tortor elementum se